One of the key elements of the REdao protocol is the Treasury: that’s where the reclaimed and bonded SOL flows as it enters the protocol. It’s the liquidity that is used to derive and support the Floor Price.

It’s also a war chest that, if managed correctly, will future proof REdao and contribute to its success — through generated yield as well as the development it finances. With great power comes great responsibility, and this is why we approach the Treasury Management subject with extra care and attention.

It is important to note that, SOL flowing into the REdao protocol is split in two ways: the majority flows to the Treasury, while a small part goes to the Development Fund. The initial rate will be 90% and 10% respectively. Following the first Halving and advance to the 2nd Epoch, this ratio will change to 95% and 5%.

Note that:

- The Treasury is comprised of the Treasury Reserve and the Treasury Surplus.

- The Development Fund will be used to cover ongoing development costs and operational expenses.

Floor Price

The pillar of REdao tokenomics is the Floor Price. While this topic is often and deservedly met with a lot of scrutiny — REdao has taken measures to ensure the reality and sustainability of this mechanism. There are several distinctive characteristics to clarify early on:

- Floor Price is the price at which the REdao Treasury Reserve can purchase all $RE tokens in existence.

- Initially, this Floor Price will be a soft lower bound — meaning that the market price could dip momentarily below the floor price. As the Treasury Reserve grows and stabilizes, this mechanism will shift to be programmatically enforced.

- Floor Price will be denominated in SOL only. This means that the Floor Price could fluctuate greatly in terms of USD as the underlying SOL price fluctuates. This also allows for RE to act as a synthetic leveraged bet on SOL. Additionally this ensures, regardless of the performance of SOL/USD, that RE/SOL can trend upwards.

- Tokens purchased by REdao at or below the Floor Price will be burnt out of circulation — adding a deflationary nature and benefiting long term holders.

The Floor Price will be calculated using the following equation:

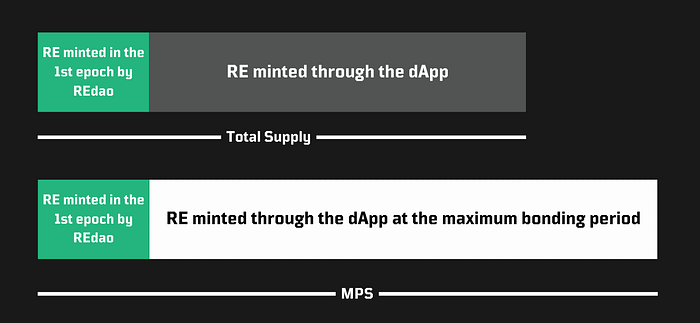

Treasury / MPS [Maximum Potential Supply] = Floor Price

Treasury Reserve / Total Supply = Floor Price

Treasury Reserve

The Treasury Reserve will be used to enforce the Floor Price and must therefore be managed conservatively, going after the safest yield on Solana: staked SOL. As long as Solana produces blocks, staked SOL and its Liquid Staking Derivatives will outperform the base asset. More about this mechanism can be read in the Marinade docs.

We will manage that SOL to take advantage of yield [and airdrop] opportunities across DeFi protocols. That might include:

- Marinade

- Jito

- LST LPing

- Kamino Vaults

- MarginFi

- Drift

- Banx

- and more

Treasury Surplus

Due to varying bonding periods and Maximum Potential Supply [MPS] the Treasury will operate at a surplus. It means that REdao will be able to purchase all RE at the Floor Price while having liquidity leftover, which is henceforth referred to as the Treasury Surplus.

MPS assumes maximum Bonding period [at 1.088 RE emissions multiplier] for all the SOL flowing into the protocol. Naturally, not every user will choose this option. This fact, combined with a large % of $RE tokens minted by REdao in the 1st Epoch being locked out of circulation for 6–12 months, let us assign the Treasury Reserve and Treasury Surplus split to be 90% and 10% respectively.

Revenue generated and held by the Treasury Surplus will be periodically rebalanced and added to the Treasury Reserve, consequently pushing the Floor Price upwards . However, given the composition of revenue streams in the Treasury Surplus, this pool will be irregular and less deterministic in terms of value added to the Floor Price.

It is important to emphasize that the Floor Price is calculated and enforced by the Treasury Reserve and not the Treasury Surplus. This means that the Floor Price can only benefit from the growth of this surplus; the performance of the Treasury Surplus will not negatively affect the Floor Price of RE in any way.

Treasury Surplus Management

The Treasury Surplus is where REdao will take less conservative, directional bets. We believe that the Solana ecosystem will continue to grow and thrive, and we plan to capitalize on it.

Our investing mandate will consider tokenomics, distribution, potential risk reward, and future outlook.

The investments will be partially hedged by LPing the tokens with SOL, which also promotes healthy growth of the ecosystem.

Additionally, any revenue generated by:

- AMMs,

- REdao Pass royalties,

- New revenue streams developed through Development Fund,

- and other activities

will be added to the Treasury Surplus and the Development Fund in a 80/20 split.

Floor price enforcement

While the enforcement of RE Floor Price results in a loss of SOL from the Treasury Reserve, purchased tokens are burnt out of circulation and thus the Treasury Reserve has fulfilled its obligation. This results in a proportional net benefit for the protocol, the token and its holders. Initially, while the floor price is soft and not programmatically enforced, REdao will employ multiple strategies to defend the floor price of RE. These strategies will be adaptable and monitored closely to provide deep liquidity for RE. These will be:

- Limit bids at and below the floor price.

- If/when the market price goes 1% below the floor price — REdao will activate a TWAP in order to ensure parity between the market price and the Floor Price.

Further comments

The nature of the Treasury Reserve being comprised of LSTs, results in several additional benefits and implications which may not be immediately apparent on the surface:

- REdao Treasury Reserve will actively contribute to the decentralization and security of the Solana, the underlying network, creating a symbiotic relationship between RE and SOL.

- Staked SOL naturally outperforms naked SOL, resulting in a passively growing Treasury Reserve in terms of SOL — the denomination of RE. This means that as long as the Solana network continues to produce blocks then, theoretically, every epoch (roughly 2–3 days) the Floor Price of RE denominated in SOL can be incremented upwards.

- The low risk and deep liquidity of LSTs provides an additional benefit — once the Floor Price of RE shifts to being programmatically enforced it will allow for low risk loans using RE as collateral in the Solana DeFi ecosystem.

- REdao Treasury will benefit from LST incentive programs, potentially resulting in additional revenue being added to the Treasury Surplus and subsequently the Treasury Reserve.

Closing comment

REdao is on a journey of continuous improvement and iteration. As our community grows and matures, we’re open to contributions and suggestions. This collaborative approach is key to fostering our community’s growth, paving the way for a future where REdao evolves into a fully decentralized and autonomous organization.